Home equity loans are closely tied to prime rates, but you might be able to negotiate better rates by shopping around. The rates for home equity lines of credit vary by Lender, as well as by your Credit score and the Draw period. Find out how to get the best home equity credit deal and make the most of it.

The prime rate is closely tied to interest rates on home equity loans of credit

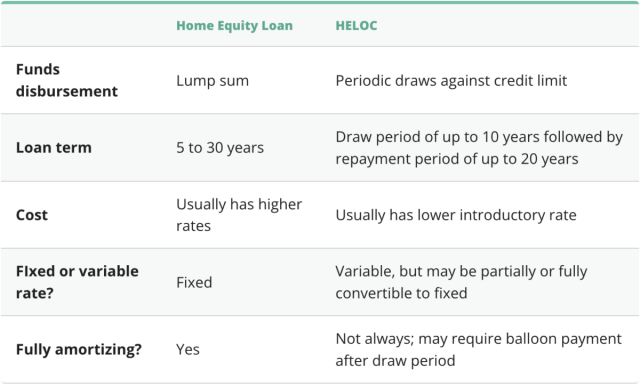

You can borrow against your equity with home equity loans or second mortgages. These loans must be repaid within a set time frame, often with monthly payments. Lenders could foreclose if you can't make the payments. The interest rate you pay on a home equity loan will depend on a number of factors, including your income and credit history. Most lenders prefer to lend to people who have at least 80 percent equity in their home.

A home equity line is an option for those who are looking for a flexible, low-interest home equity loan. These lines of credit are great for consolidating higher-interest debts or large expenses. You can make interest payments on these lines of credit tax-deductible. Many lenders offer lower interest rates for home equity lines than other loans.

Lenders can offer better deals

You should shop around for the best HELOC rate when you are looking to get one. The national economy may affect the prime rate. Variable interest rates are often charged by lenders. They will usually charge a prime plus a margin. The margin you pay will vary depending on your qualifications and other factors. If you are able to find a good deal, you can save money on the loan.

Credit score is an important factor when considering HELOC rates. To qualify for the best rates, you must have a credit score of at least 740. Some lenders have a higher credit score limit, so be sure to check with the lender before applying. Most lenders offer better deals to borrowers who have less than 70% equity in their home.

Credit score influences interest rate

You need to understand how your credit score affects the prime rate if you are thinking of applying for a HELOC. Your credit score is a major factor in getting the best rate possible, and the higher your score, the lower the interest rate will be. Check your credit reports from all three credit bureaus to determine your score. Do your best to improve your credit score before you apply. There are many things you can do to improve your score.

Your credit score and your loan-to-value ratio are the two factors that determine the interest rate for a HELOC. This ratio can be adjusted by making on-time payments, keeping your credit card balances low and paying off your home loan.

Interest rate affects draw period

You should look at the draw period when applying for a HELOC. This is the time during which the loan's interest rate fluctuates. After the draw period expires, you'll have to repay principal and interest. This could affect your rate or payment amount.

The draw period will be notified by most lenders approximately six months prior to it actually begins. To find out the draw period, you can contact the lender's customer support department. Most borrowers have to make only interest payments during the draw period. To reduce your borrowing costs while reducing the time it takes to repay, you can pay off the principal amount.

FAQ

What are the top three factors in buying a home?

The three most important things when buying any kind of home are size, price, or location. The location refers to the place you would like to live. Price refers the amount that you are willing and able to pay for the property. Size is the amount of space you require.

What is a Reverse Mortgage?

A reverse mortgage lets you borrow money directly from your home. This reverse mortgage allows you to take out funds from your home's equity and still live there. There are two types: government-insured and conventional. With a conventional reverse mortgage, you must repay the amount borrowed plus an origination fee. FHA insurance will cover the repayment.

How long does it take to sell my home?

It all depends on several factors such as the condition of your house, the number and availability of comparable homes for sale in your area, the demand for your type of home, local housing market conditions, and so forth. It may take 7 days to 90 or more depending on these factors.

How can I determine if my home is worth it?

If your asking price is too low, it may be because you aren't pricing your home correctly. If your asking price is significantly below the market value, there might not be enough interest. Our free Home Value Report will provide you with information about current market conditions.

Statistics

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

External Links

How To

How to Locate Houses for Rent

People who are looking to move to new areas will find it difficult to find houses to rent. Finding the perfect house can take time. There are many factors that can influence your decision-making process in choosing a home. These factors include location, size and number of rooms as well as amenities and price range.

To make sure you get the best possible deal, we recommend that you start looking for properties early. Also, ask your friends, family, landlords, real-estate agents, and property mangers for recommendations. This will allow you to have many choices.