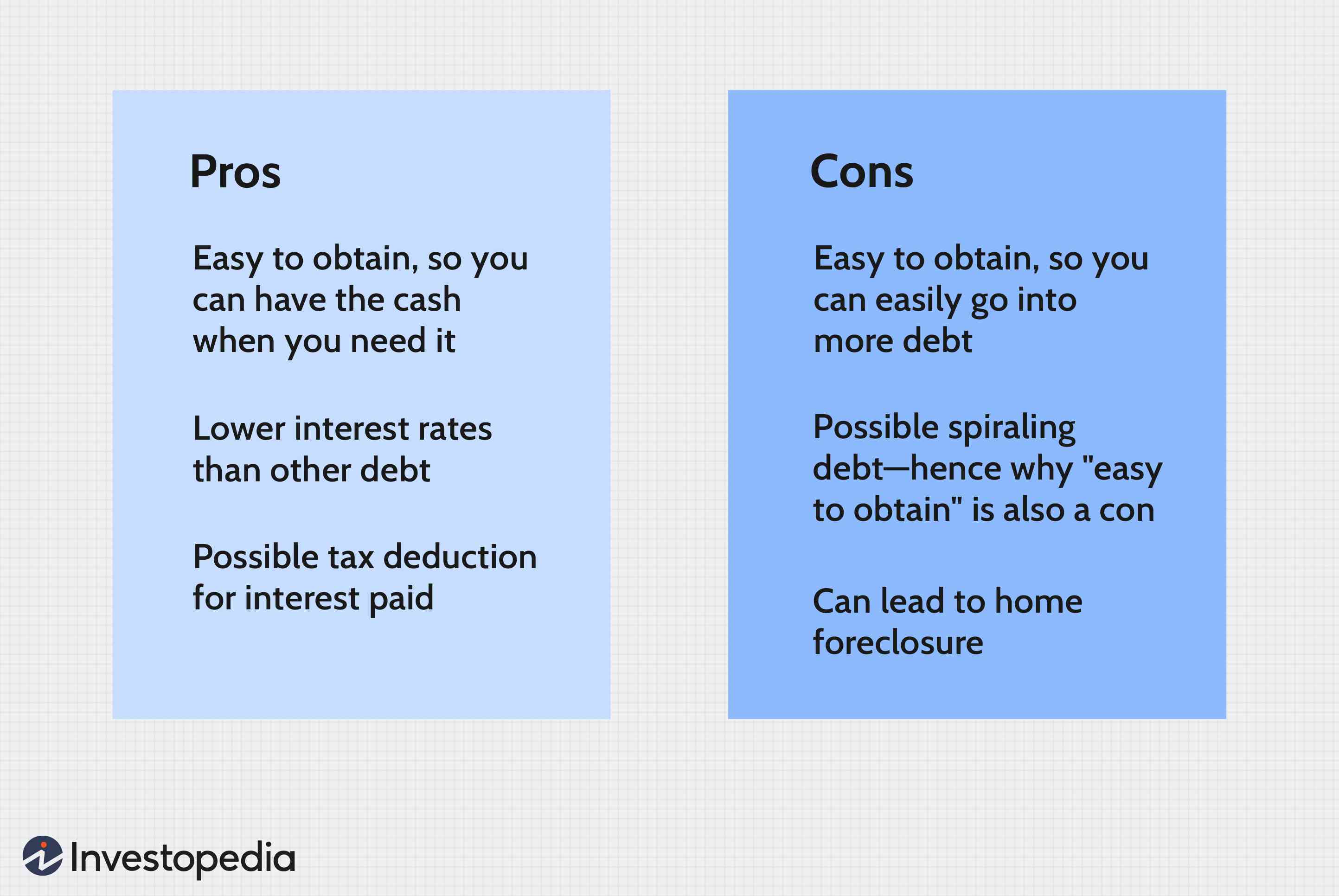

FHA loans are mortgage insurance. Most borrowers have to purchase this type of mortgage insurance. However, they may cancel the policy when they reach a certain level of equity in their house. Mortgage insurance policies can be tax-deductible. It is important to fully understand the terms and options of your mortgage insurance policy before you decide to sign up.

Single-pay Mortgage Insurance

FHA single-pay mortgage insurance is a cost-effective way to reduce your monthly mortgage insurance. If you qualify for an FHA loan, you will have to pay this insurance if you have less than 20% equity in your home. The FHA allows you to cancel this premium if you have 20% equity in your home. A typical FHA mortgage insurance policy will cost you between 0.85 percent and 1.05 percent a year, depending on the amount of the loan and the length of the mortgage term.

FHA loans offer single-pay insurance that is popular with first-time homebuyers. This mortgage insurance requires a minimum down payment of $7,000, or $40,000. This lowers the upfront cost of mortgage insurance for most borrowers. The loan amount and down payment will determine the premium.

Mortgage insurance with tax-deductible coverage

Tax-deductible mortgage insurance for FHA loans allows you to save on your mortgage insurance premiums. The premium is paid in two installments: one lump-sum payment when you close your loan. The other amount is paid monthly as part the normal loan payments. Each month, your premium payment is calculated as a percentage of your average outstanding mortgage balance. You then divide that amount by 12 to get your monthly premium.

Mortgage insurance for FHA loans isn't required for all FHA loans, but it can help you avoid paying for a large upfront premium. This can add up quickly, especially if you need to refinance your loan. FHA loans do not require mortgage insurance. After you pay it off, however, you can cancel it.

Requirements regarding down payment

Borrower is responsible to pay FHA mortgage insurance. This insurance costs 1.75% of the loan amount. The borrower will have to pay this premium up-front. This premium will be eliminated once the borrower has attained 20% equity in their home. However, the borrower will need to pay an annual MIP (mortgage insurance premium) of 0.45% - 1.05% of the loan amount multiplied by 12 months.

An FHA mortgage insurance loan is available to those who don't have enough money for a 20% downpayment. This loan requires a five-thousand dollar upfront mortgage insurance premium. Monthly payments will be made of this amount for the duration of the loan. The mortgage insurance premium will also vary depending on the size of the loan and the amount of the down payment you have. The MIP will be paid for only 11 years for borrowers who have a minimum of 10% downpayment. Those with less than 10% will have to pay it the entire loan term.

Loan limits

FHA loan limits for single family homes differ by county and metro statistical area. They typically range from $400,000 to $990,000. In more expensive areas, they are higher. Congress has set FHA loan limits in order to assist Americans with homeownership. They are more flexible than other criteria, which require lower credit scores and smaller down payment requirements.

The mortgage insurance premium is typically equal to one percent of the loan amount. For a loan of $250,000, that means a borrower would pay $4,375 in up-front premiums. If a borrower owns more than 10% of the home's equity, they can cease paying mortgage insurance. A conventional or jumbo loan will be required if the equity in the home is lower.

FAQ

Should I rent or buy a condominium?

Renting may be a better option if you only plan to stay in your condo a few months. Renting can help you avoid monthly maintenance fees. A condo purchase gives you full ownership of the unit. The space can be used as you wish.

Can I buy my house without a down payment

Yes! There are many programs that can help people who don’t have a lot of money to purchase a property. These programs include FHA, VA loans or USDA loans as well conventional mortgages. You can find more information on our website.

How much money do I need to save before buying a home?

It depends on how long you plan to live there. Save now if the goal is to stay for at most five years. But, if your goal is to move within the next two-years, you don’t have to be too concerned.

Is it possible fast to sell your house?

It might be possible to sell your house quickly, if your goal is to move out within the next few month. However, there are some things you need to keep in mind before doing so. First, find a buyer for your house and then negotiate a contract. Second, prepare your property for sale. Third, you need to advertise your property. You must also accept any offers that are made to you.

Are flood insurance necessary?

Flood Insurance protects you from flooding damage. Flood insurance helps protect your belongings and your mortgage payments. Learn more information about flood insurance.

Statistics

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

External Links

How To

How to Find Houses to Rent

Finding houses to rent is one of the most common tasks for people who want to move into new places. However, finding the right house may take some time. When choosing a house, there are many factors that will influence your decision making process. These factors include the location, size, number and amenities of the rooms, as well as price range.

To make sure you get the best possible deal, we recommend that you start looking for properties early. Consider asking family, friends, landlords, agents and property managers for their recommendations. This will give you a lot of options.