When deciding whether to obtain a home equity line of credit or a loan, you will have to consider several factors. These factors include tax perks, terms, and interest rates. You should also be familiar with the terms and fees of your lender. It comes down ultimately to your personal circumstances and how you view the situation.

Tax perks

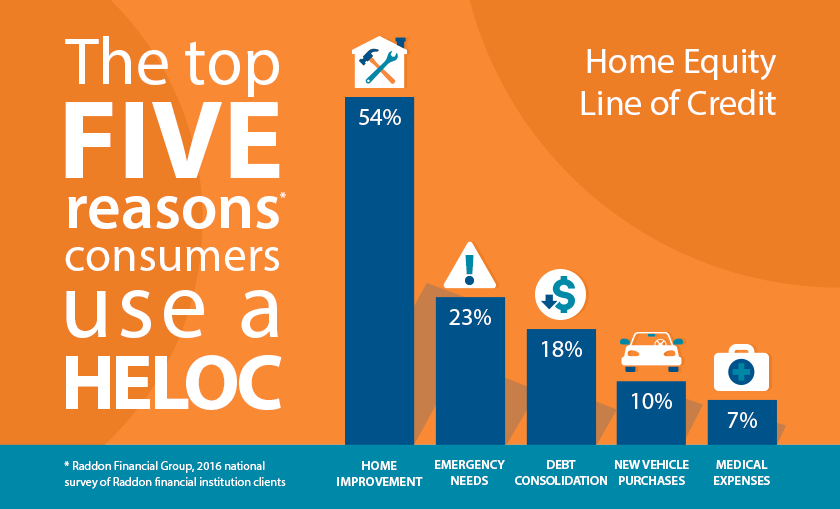

A home equity loan is a loan that you can use to finance improvements or repairs to your primary residence. Tax-deductible for loans that exceed the standard deduction. Before making any decision, consult a tax advisor.

The tax benefits of a home equity loans include low interest rates. Your home equity loan interest can often be deducted. If you are taking out a large loan, the standard deduction will be sufficient. However, it is advisable to itemize all deductions.

Rates of interest

You should consider your financial situation when deciding between a loan and a home equity credit line of credit. A home equity line credit might be the best option for you if you need money to accomplish a specific goal. These loans are usually long-term and based on your home's value. If you have high credit scores, you may qualify for a lower rate than a loan.

While the interest rates on home equity line of credit and loans are similar, one factor that makes them different is the Annual Percentage Rate (APR). The APR represents the annual interest rate that you will pay for the loan. The better the APR is, the lower it will be. Add up the interest rates and points (1 percent) to calculate the APR. You can then compare offers once you have these numbers.

Lenders' terms

One of the biggest differences between a home equity line of credit and a loan is the interest rate. Variable interest rates on home equity lines of credit can fluctuate and change throughout the term of the loan. The interest rate is linked to a benchmark, such the U.S.Prime Rate, currently at 3.5% as of the writing of this article. A margin (or profit margin) will be added to the variable interest rate by the lender. These are important things to keep in mind if the goal is to get the best possible interest rate.

Lenders may vary in the terms and rates of a loan or home equity line credit. Before signing any documents or entering into any agreement, prospective borrowers should be sure to fully understand the terms. In addition, consider how much you need and how you'll use the money. It is important to evaluate the interest rate, monthly payments, as well any tax benefits associated with a home equity line.

Revolving credit line

A home equity loan can help you finance a major purchase, or pay monthly bills. These loans are structured like credit cards, but have different features. For example, home equity loans are often offered at lower interest rates and have more flexible repayment terms. These features make them an attractive option for borrowers looking to consolidate debt. The home equity line allows you to borrow more money than traditional loans.

Each option has advantages and disadvantages. The principal difference between a house equity loan and a house equity line of credits is the interest rate. A home equity line is credit that is based on equity in your home. The money is not due until you use it. Home equity lines of credit allow you to borrow up to the amount that you need and make monthly payments as needed. Home equity loans typically have lower interest rates that credit cards. The interest on home equity loans are often exempt from tax.

Liquidity

A home equity loan of credit is a loan based on the amount of your home. You can use it for home improvements, unexpected costs, and education costs. A line of credit has the advantage that you only pay interest for what you use. It's easy to repay so you can access it whenever you need. A home equity credit line has many benefits.

A home equity loan of credit is very similar to a card. You have access only to a set amount of money which you can draw upon as required during the draw period. The difference is that you will never use all the available funds. You can only draw from the money at any time during the draw period, and your payments will fluctuate accordingly. Make sure to carefully compare both the terms of the products before making a decision.

FAQ

How much money do I need to save before buying a home?

It depends on how long you plan to live there. You should start saving now if you plan to stay at least five years. However, if you're planning on moving within two years, you don’t need to worry.

Is it cheaper to rent than to buy?

Renting is usually cheaper than buying a house. However, you should understand that rent is more affordable than buying a house. You also have the advantage of owning a home. You'll have greater control over your living environment.

How can I calculate my interest rate

Market conditions affect the rate of interest. The average interest rate over the past week was 4.39%. Multiply the length of the loan by the interest rate to calculate the interest rate. Example: You finance $200,000 in 20 years, at 5% per month, and your interest rate is 0.05 x 20.1%. This equals ten bases points.

Should I use a broker to help me with my mortgage?

A mortgage broker may be able to help you get a lower rate. Brokers have relationships with many lenders and can negotiate for your benefit. Brokers may receive commissions from lenders. Before you sign up for a broker, make sure to check all fees.

Statistics

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

External Links

How To

How to buy a mobile home

Mobile homes can be described as houses on wheels that are towed behind one or several vehicles. Mobile homes were popularized by soldiers who had lost the home they loved during World War II. People who live far from the city can also use mobile homes. Mobile homes come in many styles and sizes. Some houses are small while others can hold multiple families. Some are made for pets only!

There are two main types of mobile homes. The first type is produced in factories and assembled by workers piece by piece. This happens before the product can be delivered to the customer. A second option is to build your own mobile house. Decide the size and features you require. Next, ensure you have all necessary materials to build the house. Final, you'll need permits to construct your new home.

These are the three main things you need to consider when buying a mobile-home. Because you won't always be able to access a garage, you might consider choosing a model with more space. If you are looking to move into your home quickly, you may want to choose a model that has a greater living area. You'll also want to inspect the trailer. Problems later could arise if any part of your frame is damaged.

Before you decide to buy a mobile-home, it is important that you know what your budget is. It is important that you compare the prices between different manufacturers and models. You should also consider the condition of the trailers. While many dealers offer financing options for their customers, the interest rates charged by lenders can vary widely depending on which lender they are.

A mobile home can be rented instead of purchased. Renting allows you the opportunity to test drive a model before making a purchase. However, renting isn't cheap. The average renter pays around $300 per monthly.