A bi-weekly mortgage payment plan allows for mortgage loans to be paid twice per month instead of once per week. Other payment options for mortgages include biweekly or semi-monthly payments, as well as biweekly and accelerated biweekly payments. This payment plan is offered by third-party companies for a fee.

Benefits from bi-weekly mortgage payment

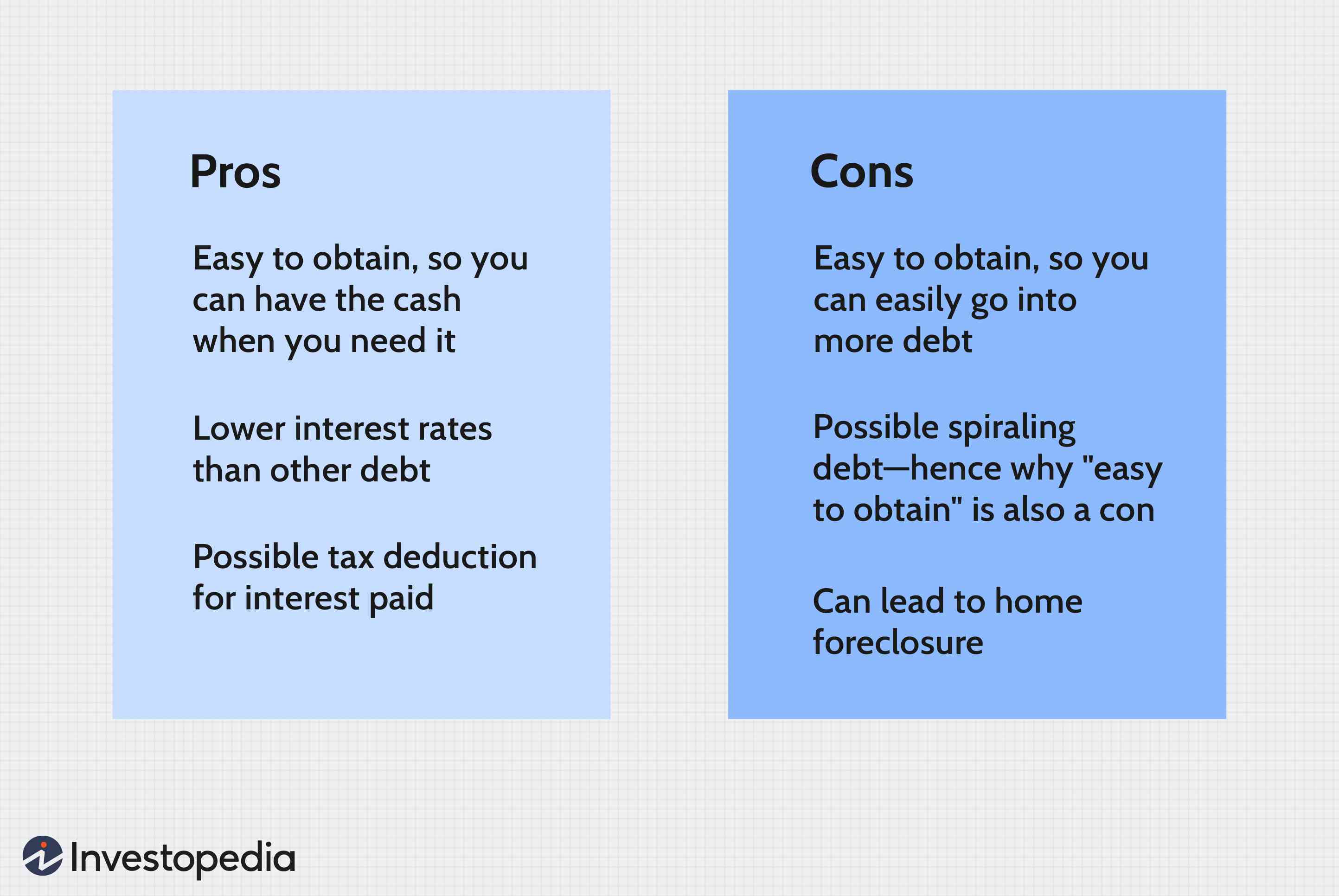

You can save a lot money by paying your mortgage bi-weekly, but it can also impact your monthly budget. Changes to the payment plan can be costly so talk to your lender before changing. It's also possible that your lender will charge you a prepayment penalty if you fail to meet the new schedule. If this happens, the prepayment penalty may exceed the savings you'd make by changing to bi-weekly mortgage payments.

The bi-weekly payment of your mortgage can save you thousands in interest. These savings depend on the loan amount, interest rate, term, and other factors. Calculate how much you can save by switching to biweekly mortgage payments using a mortgage calculator.

Cost to switch to bi-weekly mortgage payments

Bi-weekly mortgage payment might be an option if you want to save some money. These payments could help you save on interest and speed up the payment of your loan. But, each extra payment can eat away at other priorities. The extra payment can cause financial strain, regardless of whether you are saving for retirement, buying a new vehicle, or paying off high-interest debt.

You can save thousands of dollars on your mortgage by switching to bi-weekly payments. Because biweekly payments allow you to pay your loan off four years earlier, This will allow you to pay off your 30-year mortgage in just 22 years.

Alternatives to bi-weekly mortgage payments

You can coordinate your monthly expenses and pay your mortgage bi-weekly. Bi-weekly payments are much lower than monthly payments. They don't require you to be disciplined in saving or planning. Of course, you should also be aware of the potential for prepayment penalties. Prepayment penalties can be as high as $3,000 but they will not prevent you from paying off your mortgage faster.

Bi-weekly mortgage payments can be a great option if you want to make your mortgage more quickly. Instead of making a single payment each month, you will be making half the amount every two week. You'll be able to pay your mortgage off faster and save lots of interest. The biweekly payments will also help you pay off your mortgage quicker and you'll be able save more money by reducing the interest rate and delaying your monthly payment for longer periods of time.

For people who don’t like missing payments, bi-weekly payment is also an option. A $1,000 payment made every two weeks adds up to $26,000 by the end of the year. They can help you significantly increase your mortgage payoff because they follow a calendar that is yearly.

FAQ

Should I use a broker to help me with my mortgage?

Consider a mortgage broker if you want to get a better rate. Brokers work with multiple lenders and negotiate deals on your behalf. However, some brokers take a commission from the lenders. Before you sign up for a broker, make sure to check all fees.

Is it possible fast to sell your house?

You may be able to sell your house quickly if you intend to move out of the current residence in the next few weeks. You should be aware of some things before you make this move. First, find a buyer for your house and then negotiate a contract. Second, you need to prepare your house for sale. Third, you must advertise your property. You must also accept any offers that are made to you.

How can you tell if your house is worth selling?

If you have an asking price that's too low, it could be because your home isn't priced correctly. You may not get enough interest in the home if your asking price is lower than the market value. For more information on current market conditions, download our Home Value Report.

What are the drawbacks of a fixed rate mortgage?

Fixed-rate loans have higher initial fees than adjustable-rate ones. Additionally, if you decide not to sell your home by the end of the term you could lose a substantial amount due to the difference between your sale price and the outstanding balance.

What should you look out for when investing in real-estate?

It is important to ensure that you have enough money in order to invest your money in real estate. If you don’t save enough money, you will have to borrow money at a bank. You also need to ensure you are not going into debt because you cannot afford to pay back what you owe if you default on the loan.

It is also important to know how much money you can afford each month for an investment property. This amount should include mortgage payments, taxes, insurance and maintenance costs.

You must also ensure that your investment property is secure. It would be best to look at properties while you are away.

How many times can I refinance my mortgage?

This will depend on whether you are refinancing through another lender or a mortgage broker. In both cases, you can usually refinance every five years.

How can I calculate my interest rate

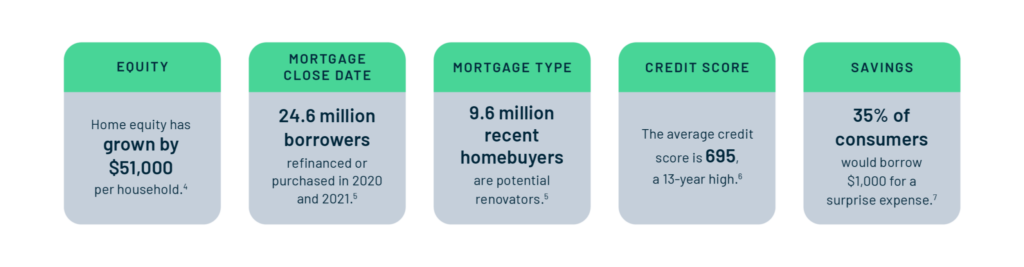

Market conditions affect the rate of interest. The average interest rate for the past week was 4.39%. To calculate your interest rate, multiply the number of years you will be financing by the interest rate. For example, if $200,000 is borrowed over 20 years at 5%/year, the interest rate will be 0.05x20 1%. That's ten basis points.

Statistics

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

External Links

How To

How to Buy a Mobile Home

Mobile homes are houses built on wheels and towed behind one or more vehicles. Mobile homes were popularized by soldiers who had lost the home they loved during World War II. People today also choose to live outside the city with mobile homes. These houses come in many sizes and styles. Some houses are small, others can accommodate multiple families. Some are made for pets only!

There are two main types of mobile homes. The first type is manufactured at factories where workers assemble them piece by piece. This is done before the product is delivered to the customer. You could also make your own mobile home. You'll need to decide what size you want and whether it should include electricity, plumbing, or a kitchen stove. Next, ensure you have all necessary materials to build the house. Finally, you'll need to get permits to build your new home.

You should consider these three points when you are looking for a mobile residence. Because you won't always be able to access a garage, you might consider choosing a model with more space. If you are looking to move into your home quickly, you may want to choose a model that has a greater living area. Third, make sure to inspect the trailer. If any part of the frame is damaged, it could cause problems later.

Before buying a mobile home, you should know how much you can spend. It is important to compare the prices of different models and manufacturers. It is important to inspect the condition of trailers. Many dealerships offer financing options but remember that interest rates vary greatly depending on the lender.

It is possible to rent a mobile house instead of buying one. Renting allows the freedom to test drive one model before you commit. Renting isn’t cheap. Most renters pay around $300 per month.