When comparing 30-year mortgage rates, it is important to keep several factors in mind. These factors include your down payment amount, type of loan and credit score. When you are looking for the lowest rate mortgage, make sure to factor in the application fee and origination costs.

Rates on 30-year mortgages tend to be higher than rates on 15-year ones

Contrary 15-year mortgages with higher interest rates, 30 year mortgages will have higher total payments over the term. A Bankrate mortgage survey shows that the average fixed-rate 30-year mortgage rate is currently 3.75 percent. This rate is higher than the historic low of 2.922%, which was set for 2020. By contrast, the average 15-year mortgage rate is 2.92%.

While 30 year mortgages have higher interest rates, a longer loan period may help you save more money over time. You may be able pay your mortgage off faster if you are able to make all your payments in a shorter time frame. A 30-year mortgage also gives you more time to save for other expenses.

Down payment

Paying 20% down on a 30 year mortgage can have many benefits. This not only lowers your monthly mortgage payment but also shows you are serious about buying a property. It's obvious that rational people wouldn't make an investment in property they would have to give up in a poor economy.

It is important that you consider the size and amount of your savings when making a downpayment on your mortgage. A minimum of 3% is required for most mortgages, but you can choose to pay as much as 20%. Your individual circumstances will dictate the amount of money that you can afford. A downpayment calculator can help determine how much money to save each month.

Types of loans

When looking for a 30-year-term mortgage, it's important you compare rates from various lenders. Rates are based on your personal credit profile and down payment amount, and they can vary widely from lender to lender. The best rates can help save you thousands of money over the life-of the loan. Make sure to shop around and check individual firms' websites for updated information.

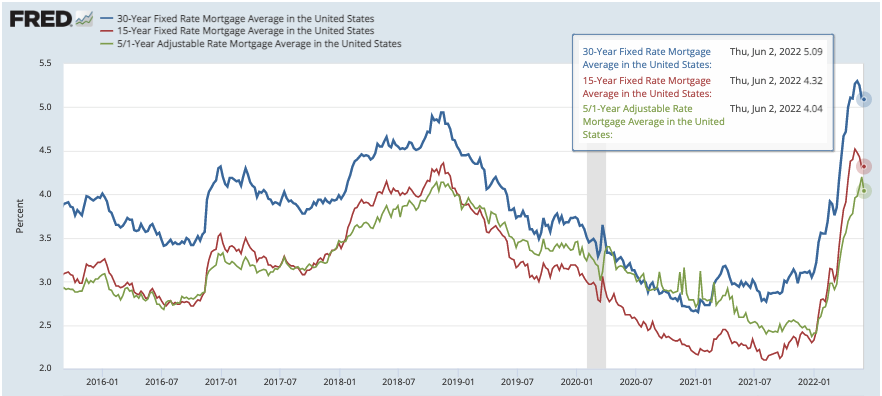

Rates on mortgages can fluctuate daily. The Federal Reserve raised rates this year for the fourth time, marking the highest increase in rates in nearly three decades. Other factors may also have an impact on mortgage rates. On September 14, the latest data showed that the average 30-year mortgage rate had increased 0.09 percent. Although home prices have not increased as fast in recent years as they did, mortgage rates could continue to be higher than the average buyer's range.

Credit score

When comparing 30 year mortgage rates, it is important to keep your credit score in mind. An algorithm determines your credit score by assigning numerical values to each item on your credit report. A lower credit score is based on late payments, non-payment and other bad behavior. Positive behavior and timely payments lead to a higher score. Also, lenders can use your credit score to determine how responsible you are. This could affect your interest rates.

Lenders base mortgage interest rates on borrowers' FICO scores. You should check your credit score before applying for a mortgage. This service is offered by most financial institutions for no cost. Lenders want to see a credit utilization rate of at least 30 percent. Another important aspect is your payment history. Your credit score is 35 percent dependent on your payment history. Your credit score is 35 percent dependent on how much you pay. Late payments remain on your credit file for seven years. However, the impact of late payments diminishes over time. You should review your credit report and take steps to correct any errors.

Interest rate index

Rates on 30-year mortgages can fluctuate often. Homebuyers have new options. Low rates lead to a rise in demand for 30-year mortgages. The opposite is true for high interest rates. A 30-year fixed interest rate mortgage is a good option as it offers a stable rate for the whole 30 year.

The current average rate for a 30-year mortgage is 6.70%. This is lower than the 7.76% long-term average. It is important to compare the daily changes with the quotes from different lenders to take advantage this low interest rate.

FAQ

How much will it cost to replace windows

Replacing windows costs between $1,500-$3,000 per window. The total cost of replacing all of your windows will depend on the exact size, style, and brand of windows you choose.

What is the average time it takes to get a mortgage approval?

It depends on several factors such as credit score, income level, type of loan, etc. It generally takes about 30 days to get your mortgage approved.

Can I get a second mortgage?

Yes. However, it's best to speak with a professional before you decide whether to apply for one. A second mortgage can be used to consolidate debts or for home improvements.

Should I rent or buy a condominium?

If you plan to stay in your condo for only a short period of time, renting might be a good option. Renting allows you to avoid paying maintenance fees and other monthly charges. A condo purchase gives you full ownership of the unit. The space is yours to use as you please.

Statistics

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

External Links

How To

How to Buy a Mobile Home

Mobile homes can be described as houses on wheels that are towed behind one or several vehicles. Mobile homes were popularized by soldiers who had lost the home they loved during World War II. People who want to live outside of the city are now using mobile homes. These houses are available in many sizes. Some houses are small, others can accommodate multiple families. There are even some tiny ones designed just for pets!

There are two types main mobile homes. The first type of mobile home is manufactured in factories. Workers then assemble it piece by piece. This takes place before the customer is delivered. A second option is to build your own mobile house. It is up to you to decide the size and whether or not it will have electricity, plumbing, or a stove. Then, you'll need to ensure that you have all the materials needed to construct the house. Finally, you'll need to get permits to build your new home.

Three things are important to remember when purchasing a mobile house. Because you won't always be able to access a garage, you might consider choosing a model with more space. If you are looking to move into your home quickly, you may want to choose a model that has a greater living area. The trailer's condition is another important consideration. You could have problems down the road if you damage any parts of the frame.

You need to determine your financial capabilities before purchasing a mobile residence. It's important to compare prices among various manufacturers and models. Also, look at the condition of the trailers themselves. Although many dealerships offer financing options, interest rates will vary depending on the lender.

You can also rent a mobile home instead of purchasing one. You can test drive a particular model by renting it instead of buying one. However, renting isn't cheap. Renters usually pay about $300 per month.