A home equity loan, also known as a HELOC, is a type of home equity line of credit. Its amount depends on several factors, including the equity in your home, your credit score, your loan-to-value ratio, and your debt-to-income ratio. You shouldn't borrow more that 90% of the home's value.

Home equity loan

Be sure to consider your specific needs before making a decision between a home-equity loan and refinance cashout. You may find that a home equity loan is a better option due to its lower interest rate, lower closing cost, and the lack of credit checks. Cash out refinance can, however, be a better option for certain purposes such as consolidating debts and replacing your existing mortgage loan.

Both options can be used by homeowners. The main difference between a loan for home equity and a refinance is that the terms of your primary mortgage will not be changed by a line of credit for home equity (HELOC). The interest you pay on a home equity loan will be independent of your primary mortgage, and it will likely come with its own terms and conditions. It is possible to deduct the interest on a HELOC. Home equity loans may also have additional costs such as closing costs and application fees.

Refinance by cash-out

A home equity loan can be a great way for you to borrow more money without the need for a second mortgage. The loan can be used for a variety of purposes, including debt consolidation, making big-ticket purchases, and making expensive home improvements. The process of cash-out refinances is usually easier if you have a low amount of debt to income ratio. So borrowers with poor credit should consider this option.

Cash-out refinances are usually more expensive and last longer than a home-equity loan. A home equity loan might be better if you have substantial equity in your property or are looking to lower your mortgage payments. Be sure to compare both options carefully before making a decision. A mortgage specialist will be able to provide the details you need to make an educated decision.

Another difference between a cash-out refinance and a home equity loan is whether or not mortgage insurance is required. Mortgage insurance is required for cash-out refinances. This protects the lender in the event of default. To be able to reach this level, you will need mortgage insurance. However, once you reach this threshold, you can usually cancel the insurance.

Home equity line credit

A home equity line of credit can be a good option for those who need additional cash. However, you should be aware that monthly payments may increase and you may have to make higher monthly payments. Refinancing your house with a cash out refinance could also alter the terms of your mortgage and increase your debt. This could put you in a difficult financial spot, particularly if your property has declined since you took out your loan.

A home equity line is best if you have major expenses and need to borrow against it. Both have their advantages and disadvantages and you should carefully weigh each option before making a decision.

If you are in need of emergency cash but have concerns about your credit, a home equity line-of-credit loan can be a good choice. Home equity credit loans will typically require a credit score of at least 580. In order to be eligible, you need to have a minimum equity of 15% in your home.

FAQ

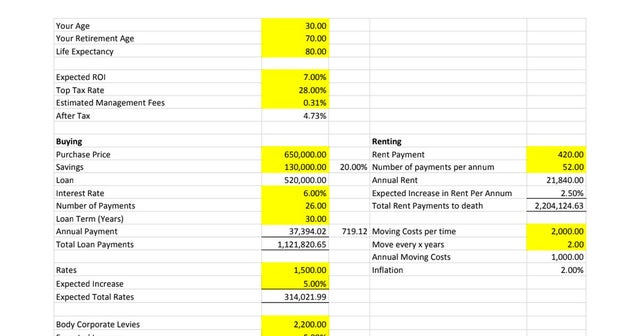

Is it cheaper to rent than to buy?

Renting is generally cheaper than buying a home. However, you should understand that rent is more affordable than buying a house. You also have the advantage of owning a home. You will be able to have greater control over your life.

Should I use an mortgage broker?

A mortgage broker is a good choice if you're looking for a low rate. Brokers have relationships with many lenders and can negotiate for your benefit. Some brokers receive a commission from lenders. Before you sign up for a broker, make sure to check all fees.

What are the pros and cons of a fixed-rate loan?

Fixed-rate mortgages guarantee that the interest rate will remain the same for the duration of the loan. You won't need to worry about rising interest rates. Fixed-rate loans also come with lower payments because they're locked in for a set term.

Is it possible fast to sell your house?

If you have plans to move quickly, it might be possible for your house to be sold quickly. But there are some important things you need to know before selling your house. First, you must find a buyer and make a contract. The second step is to prepare your house for selling. Third, you need to advertise your property. Lastly, you must accept any offers you receive.

How do I calculate my interest rate?

Interest rates change daily based on market conditions. The average interest rate over the past week was 4.39%. To calculate your interest rate, multiply the number of years you will be financing by the interest rate. For example, if $200,000 is borrowed over 20 years at 5%/year, the interest rate will be 0.05x20 1%. That's ten basis points.

Statistics

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

External Links

How To

How do you find an apartment?

Finding an apartment is the first step when moving into a new city. This takes planning and research. It involves research and planning, as well as researching neighborhoods and reading reviews. While there are many options, some methods are easier than others. Before you rent an apartment, consider these steps.

-

Online and offline data are both required for researching neighborhoods. Online resources include Yelp. Zillow. Trulia. Realtor.com. Other sources of information include local newspapers, landlords, agents in real estate, friends, neighbors and social media.

-

Find out what other people think about the area. Review sites like Yelp, TripAdvisor, and Amazon have detailed reviews of apartments and houses. You may also read local newspaper articles and check out your local library.

-

You can make phone calls to obtain more information and speak to residents who have lived there. Ask them what they loved and disliked about the area. Ask for recommendations of good places to stay.

-

Consider the rent prices in the areas you're interested in. If you are concerned about how much you will spend on food, you might want to rent somewhere cheaper. If you are looking to spend a lot on entertainment, then consider moving to a more expensive area.

-

Learn more about the apartment community you are interested in. What size is it? What's the price? Is it pet-friendly What amenities does it have? Are you able to park in the vicinity? Do tenants have to follow any rules?