It is important to understand the duration of a foreclosure on credit reports. However, foreclosures can negatively impact your credit. It all depends on the time it was done. A foreclosure can stay on your credit record for up to seven years. However, some bankruptcies and medical debt take longer to disappear from your credit report. A foreclosure can cause a significant impact on your credit score up to seven years after you move out of a rental or bought a house.

What length of time does a foreclosure stay on my credit report?

Your credit report will still have foreclosures seven years after the date of foreclosure. You may have difficulty getting credit cards, home loans, or renting apartments if you have foreclosures and other negative information on your credit report. Also, foreclosures can impact your job prospects.

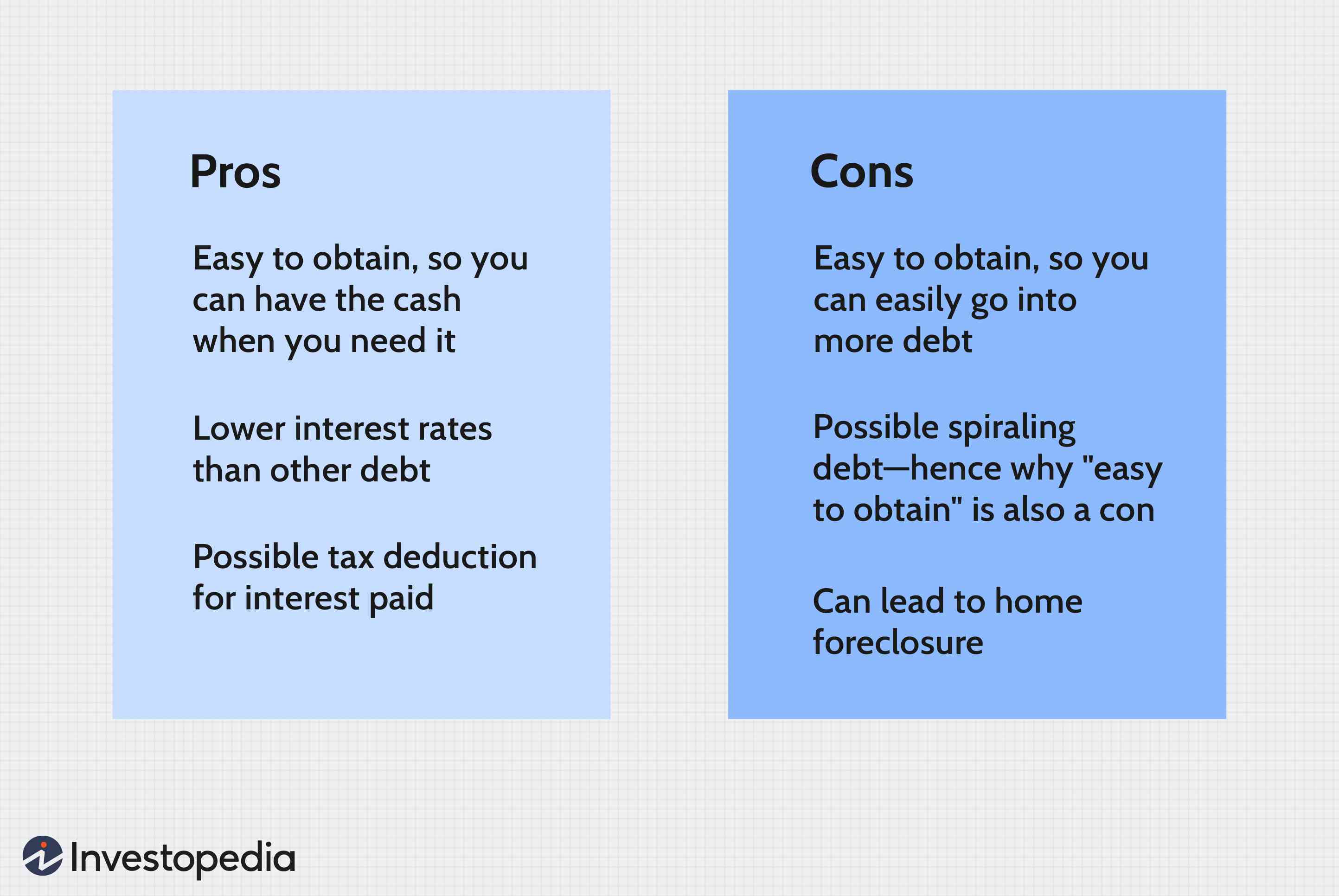

US foreclosures are a common occurrence. They can be stressful and frustrating. One of the consequences of foreclosure is lower credit scores and higher costs for insurance. Fortunately, there are ways to minimize the impact of a foreclosure on your credit.

The foreclosure can be disputed. You can file a dispute to the three major credit agencies to have the foreclosure lifted. To do so, you must send a written notice. Once you file your dispute, you should receive a response within thirty days. After reviewing the dispute credit bureaus will have the task of verifying the entry and making corrections if needed. The bureaus may also remove the entry completely.

Credit scores affected by a foreclosure

It can have devastating effects on your credit score. A negative credit record will remain on your credit report for seven year. Credit scores will decline if you have had a foreclosure or other negative credit history. You will also be less likely to get home loans, credit cards, or other types of loans. You will have a lower chance of landing a job, or renting an apartment.

If you are facing foreclosure, you should take action to repair your credit. Contact your lender immediately to inform them that you have difficulty paying your mortgage payments. Your lender may be willing to work with you. Several missed payments can trigger foreclosure. If you're unable to pay these payments, you could face foreclosure for up to seven years.

To buy a new house, you will need to get another mortgage after a foreclosure. Your credit score will be less affected by a new mortgage than from a foreclosure. However, you might need to look for another mortgage lender. Many lenders look at credit reports before making a loan decision. Higher risks are generally associated with people with lower credit scores.

Renting a house after a foreclosure has an impact

It is possible to have concerns about your rights and obligations when renting out a home after a foreclosure. It is important to understand the rights of the new and old owners. You must ensure that your lease is honored by the new owner. The new owner should also provide the same services as the previous landlord.

First, you must understand that investors can often purchase foreclosed homes. This means that they were hoping to rent out the property for a profit. These individuals lost their investment properties due both to rising mortgage interests rates and a drop in housing value. The foreclosed properties are sold to the highest bidder. A service company may be hired by the new owners to maintain the rental property.

Another concern about foreclosures is their potential impact on neighborhoods. Foreclosures can cause damage to the neighborhood and even lead to eviction. This is not only damaging to tenants, but can also have a negative impact on the renter's credit. It can cause them to lose their security deposit and make it more difficult to find housing elsewhere.

FAQ

What should I look for in a mortgage broker?

People who aren't eligible for traditional mortgages can be helped by a mortgage broker. They search through lenders to find the right deal for their clients. Some brokers charge a fee for this service. Others offer free services.

What are the three most important factors when buying a house?

When buying any type or home, the three most important factors are price, location, and size. Location refers the area you desire to live. Price is the price you're willing pay for the property. Size refers how much space you require.

What is the average time it takes to sell my house?

It depends on many different factors, including the condition of your home, the number of similar homes currently listed for sale, the overall demand for homes in your area, the local housing market conditions, etc. It may take 7 days to 90 or more depending on these factors.

Is it better for me to rent or buy?

Renting is typically cheaper than buying your home. However, renting is usually cheaper than purchasing a home. You also have the advantage of owning a home. For instance, you will have more control over your living situation.

Statistics

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

External Links

How To

How to locate an apartment

Finding an apartment is the first step when moving into a new city. This requires planning and research. This involves researching neighborhoods, looking at reviews and calling people. You have many options. Some are more difficult than others. These are the steps to follow before you rent an apartment.

-

Data can be collected offline or online for research into neighborhoods. Online resources include Yelp. Zillow. Trulia. Realtor.com. Offline sources include local newspapers, real estate agents, landlords, friends, neighbors, and social media.

-

Review the area where you would like to live. Yelp. TripAdvisor. Amazon.com have detailed reviews about houses and apartments. You might also be able to read local newspaper articles or visit your local library.

-

You can make phone calls to obtain more information and speak to residents who have lived there. Ask them what the best and worst things about the area. Ask for recommendations of good places to stay.

-

Check out the rent prices for the areas that interest you. If you think you'll spend most of your money on food, consider renting somewhere cheaper. Consider moving to a higher-end location if you expect to spend a lot money on entertainment.

-

Find out about the apartment complex you'd like to move in. It's size, for example. What price is it? Is it pet-friendly? What amenities does it offer? Is it possible to park close by? Do you have any special rules applicable to tenants?