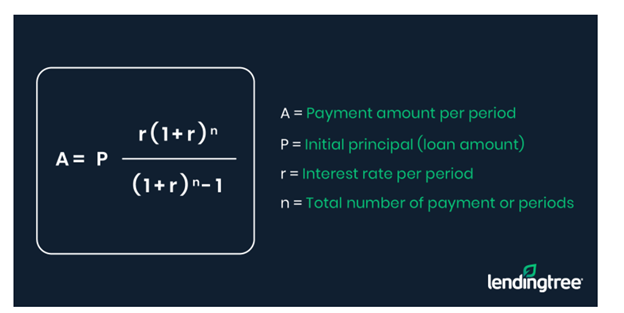

A mass mortgage calculator is a useful tool that allows you to compare the costs of renting and owning a home. There are many factors that affect the interest rate on mortgages. They fluctuate daily so your actual payment will vary. Some of these variables are beyond your control. Other factors are more easily controlled. With a mass mortgage calculator, you can get an estimate of your maximum monthly payment based on a variety of variables, including the purchase price, down payment, and interest rate. This calculator will also consider taxes and insurance.

Based on the purchase price, downpayment, loan term and interest rate, this calculator estimates your maximum monthly mortgage payment.

Mass mortgage calculators require you to input your purchase price (down payment), loan term, interest, rate and home's valuation. This information will be used by lenders for determining your maximum monthly payment. This information is used by lenders to determine your maximum monthly mortgage payment. The calculator will also factor in any homeowners' association fees.

You can use a mortgage calculator to compare the monthly payments for different home values. Depending upon your financial situation, you might be able to choose different loan terms and set down different amounts. You can also play around with the interest rate, which will also affect your monthly payment.

Includes taxes and insurance

The Massachusetts Mortgage Calculator can help you estimate your monthly payment, including insurance or PMI. You can also enter additional payments like bi-weekly payments or home owners association fees. A schedule of amortization is included in the calculator so that you can see how long your mortgage will be paying off. You can export or print this information to an Excel spreadsheet, so you can examine your payment history.

You can also use the mortgage calculator to calculate how much money you could save by making additional payments throughout the term of your mortgage. Even a single extra payment can cut down your term. You can explore various mortgage scenarios to determine if they are feasible and financial wise. You should verify all information from a mortgage calculator before you make any final decisions.

This does not make you eligible for a loan.

Although mortgage calculators can estimate your monthly mortgage payment they don't pre-qualify for loans. The interest rates are affected by many factors. The calculator uses information like your credit score, down payments, and loan types to calculate the maximum monthly installment. This calculator allows you to assess your financial situation and determine if you have the ability to buy a house.

You must enter your entire income and all debt when using a mass-mortgage calculator. Your total monthly income should be at least three times your current monthly debt payment, as this will give you a good idea of whether you can afford a mortgage. As the down payment is the largest upfront payment, it is also important to determine how much you are able to afford.

How to adjust the default values on the mortgage calculator so that they reflect your current situation

A mortgage calculator will give you an idea of what you could afford to buy a home every month. These inputs can be used as estimates, and should always be adjusted to suit your individual circumstances. You can find mortgage calculators from organizations like CoreLogic, The Tax Foundation, and Quadrant Information Services. These tools can help you budget your finances and give you an idea of your monthly payment.

The default values of a mortgage calculator are determined based on the loan term and the rate. You should choose an interest rate that corresponds to your mortgage term and budget. You should, for example, enter the average interest rate for a 15-year mortgage. By adjusting these default values, you'll be able to compare different loan terms and find a good balance.

FAQ

Can I afford a downpayment to buy a house?

Yes! There are programs available that allow people who don't have large amounts of cash to purchase a home. These programs include conventional mortgages, VA loans, USDA loans and government-backed loans (FHA), VA loan, USDA loans, as well as conventional loans. Visit our website for more information.

What should I do if I want to use a mortgage broker

Consider a mortgage broker if you want to get a better rate. Brokers work with multiple lenders and negotiate deals on your behalf. Some brokers earn a commission from the lender. Before signing up, you should verify all fees associated with the broker.

What is the maximum number of times I can refinance my mortgage?

This is dependent on whether the mortgage broker or another lender you use to refinance. In either case, you can usually refinance once every five years.

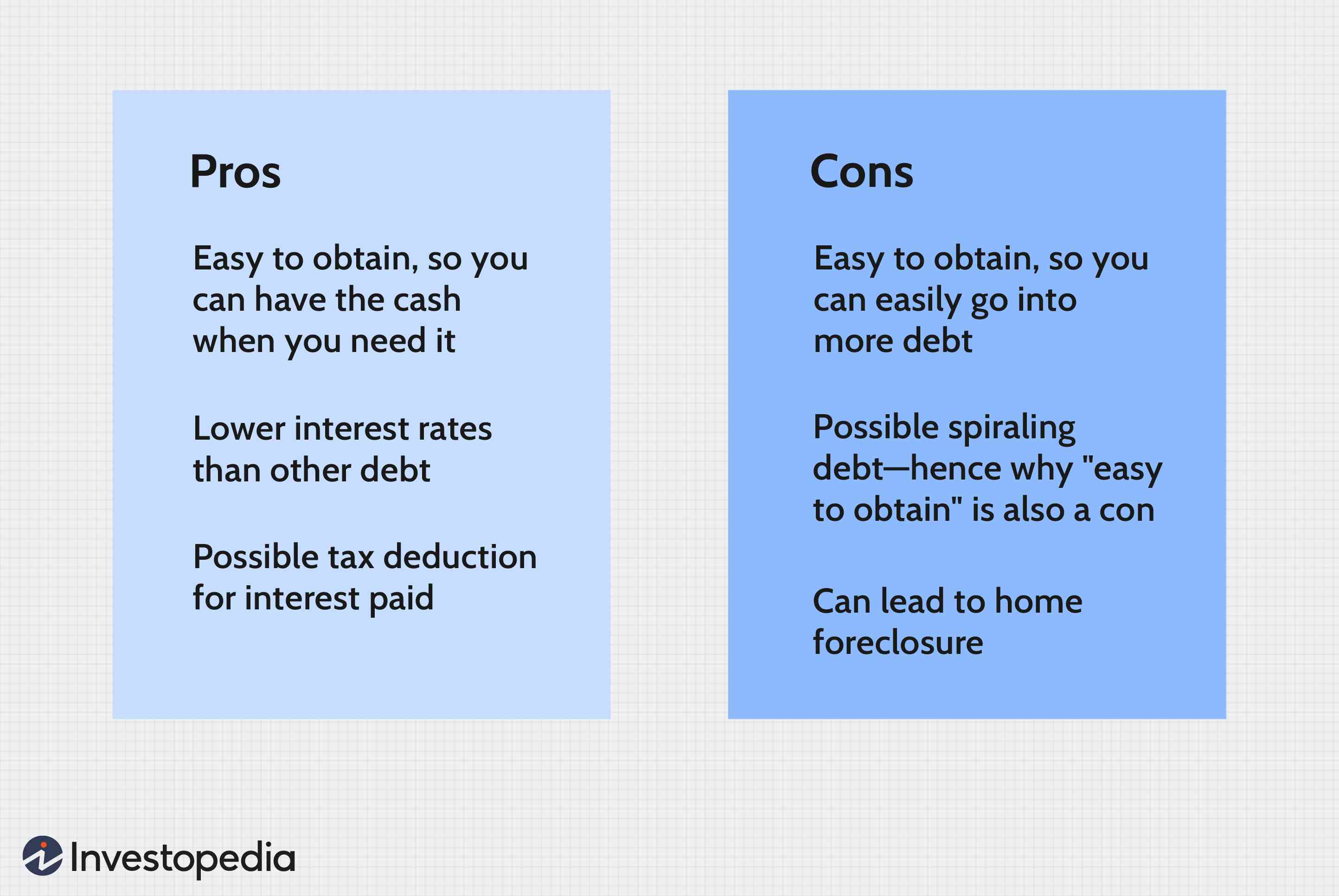

What are the pros and cons of a fixed-rate loan?

Fixed-rate mortgages guarantee that the interest rate will remain the same for the duration of the loan. This means that you won't have to worry about rising rates. Fixed-rate loans also come with lower payments because they're locked in for a set term.

How long does it usually take to get your mortgage approved?

It is dependent on many factors, such as your credit score and income level. It generally takes about 30 days to get your mortgage approved.

What is a Reverse Mortgage?

Reverse mortgages are a way to borrow funds from your home, without having any equity. It allows you to borrow money from your home while still living in it. There are two types of reverse mortgages: the government-insured FHA and the conventional. Conventional reverse mortgages require you to repay the loan amount plus an origination charge. FHA insurance covers your repayments.

What are the 3 most important considerations when buying a property?

The three most important things when buying any kind of home are size, price, or location. Location refers the area you desire to live. Price is the price you're willing pay for the property. Size refers to how much space you need.

Statistics

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

External Links

How To

How to find real estate agents

A vital part of the real estate industry is played by real estate agents. They sell homes and properties, provide property management services, and offer legal advice. The best real estate agent will have experience in the field, knowledge of your area, and good communication skills. To find a qualified professional, you should look at online reviews and ask friends and family for recommendations. Consider hiring a local agent who is experienced in your area.

Realtors work with homeowners and property sellers. A realtor's job is to help clients buy or sell their homes. As well as helping clients find the perfect home, realtors can also negotiate contracts, manage inspections and coordinate closing costs. Most agents charge a commission fee based upon the sale price. Some realtors do not charge fees if the transaction is closed.

The National Association of Realtors(r) (NAR), offers many different types of real estate agents. To become a member of NAR, licensed realtors must pass a test. A course must be completed and a test taken to become certified realtors. NAR has set standards for professionals who are accredited as realtors.